Europe’s PMI Just Hit a 10-Month Low. The ECB Now Faces an Impossible Choice.

The PMI Breakdown

What It Is

The Purchasing Managers Index is a monthly survey of business activity compiled by S&P Global. It covers manufacturing and services across the eurozone. A reading above 50 means the private sector is expanding; below 50 means it is contracting. The composite PMI at 50.5 means Europe’s economy is still growing, but only just. It takes one more bad month to tip it into outright contraction.

Why This Number Matters

The March reading missed every economist forecast. It came in at 50.5 against an expected 51.0, down sharply from 51.9 in February. That is the lowest composite PMI in 10 months and the single biggest month-on-month drop since the eurozone was dealing with the fallout from Russia’s invasion of Ukraine in 2022. France has now recorded three consecutive months below 50, meaning its private sector is in contraction. Germany slipped more than anticipated. Both declines were led by services, not manufacturing, which tells you this is a confidence and cost problem, not just an export slowdown.

What It Is Telling Us

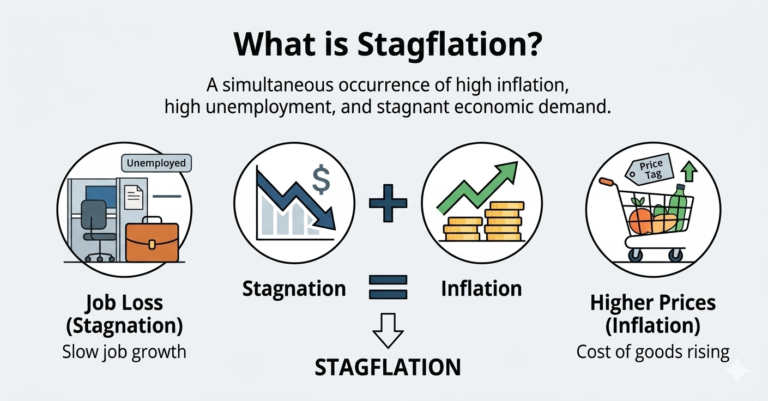

The Iran war is delivering a dual blow to Europe that textbook economics calls stagflation: rising prices on one side, stalling growth on the other. Firms reported cost increases at the fastest pace in over three years, driven by the energy spike and supply chain disruption from the Strait of Hormuz closure. Supplier delays jumped to their highest since mid-2022. Hiring was scaled back. Output expectations fell by the most since Russia invaded Ukraine four years ago.

S&P Global’s PMI price gauge now suggests eurozone inflation is running close to 3%, above the ECB’s 2% target and above the ECB’s own revised forecast of 2.6% for 2026. “The flash Eurozone PMI is ringing stagflation alarm bells,” said Chris Williamson, chief business economist at S&P Global Market Intelligence. European Commission President Ursula von der Leyen called the energy situation “critical” and demanded negotiations to end the war. Markets responded by pricing in roughly 70 basis points of ECB rate hikes by year-end.

“Firms’ costs are rising at the fastest rate for over three years amid the surge in energy prices and choking of supply chains resulting from the war. Supplier delays have jumped to their highest since mid-2022.”

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

The Nuance

50.5 is still above 50. Europe’s economy is not in recession yet. The ECB’s own revised forecasts from last week still show 0.9% growth in 2026. But that forecast was built on assumptions about how long the conflict lasts. If the Iran war extends through the second quarter, every model gets revised lower. The more immediate problem is that the ECB cannot respond the way it would in a normal slowdown. Cutting rates would ease the growth pain but would pour fuel onto an inflation fire that is already burning above target. ECB Governing Council member Boris Vujcic put it plainly: “We do not see stagflation, but the risk is moving in the direction of stagflation.”