What Is Stagflation and Why It Is Worse Than a Recession

Gas is up 16% in a week. The S&P 500 is down nearly 3% over the same period. The Fed cannot cut rates because inflation is rising. It cannot raise rates because the economy is already slowing. That combination has a name: stagflation. And it is harder to escape than a standard recession.

The Short Answer

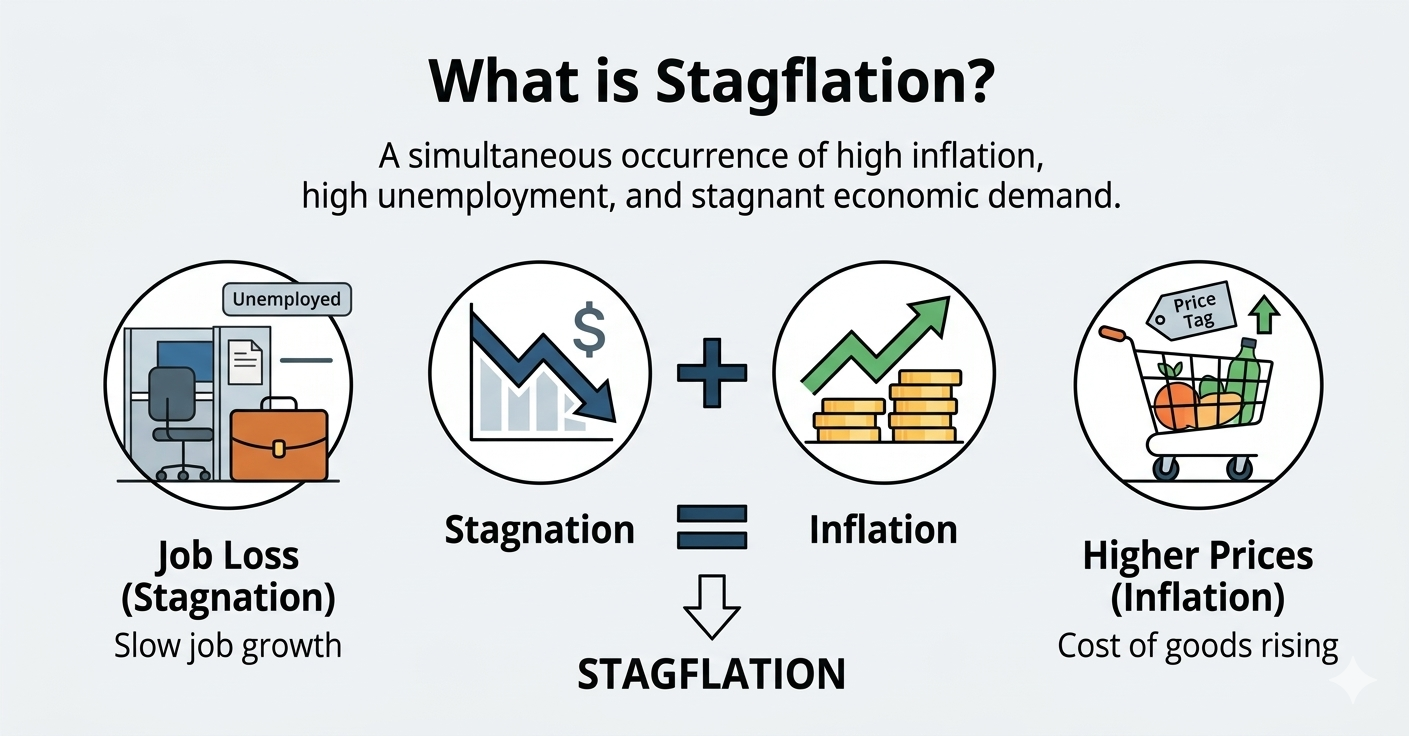

Stagflation is what happens when inflation and economic stagnation occur at the same time. In a normal recession, prices fall as demand drops and the Federal Reserve cuts interest rates to stimulate growth. The playbook is well understood and it works. Stagflation breaks that playbook. Prices keep rising even as the economy slows, which means the Fed cannot cut rates without making inflation worse and cannot raise rates without pushing the economy deeper into contraction. There is no clean move.

How It Works

Standard inflation is a demand problem. Too much money chasing too few goods. The Fed raises rates, borrowing becomes more expensive, spending slows, prices come back down.

Stagflation is a supply problem. When the cost of producing and delivering goods rises sharply (usually because of an energy shock), prices go up even as consumers pull back on spending. Businesses face higher input costs and weaker demand at the same time. They cut jobs to protect margins. The economy contracts while prices stay elevated. The Fed is now caught between two bad outcomes: fight inflation and cause a deeper recession, or support growth and let inflation run.

The last major stagflation episode was the 1970s. The 1973 OPEC oil embargo triggered a supply shock nearly identical to what the Hormuz closure is doing now. Gas prices spiked, inflation hit 12%, and US GDP contracted. It took Federal Reserve Chair Paul Volcker hiking interest rates to 20% in 1980 to finally break it. That cure caused one of the deepest recessions in modern US history.

Why It Matters Right Now

The current setup matches the early stages of a stagflationary environment. Oil has surged over 9% in a single session. Gas at the pump hit $3.48 per gallon this week, a 16% jump in seven days. At the same time, the February jobs report missed estimates by 62,000 and recession prediction markets have moved from 20% to 42% probability since January.

The Fed’s problem is identical to the 1970s bind. Core inflation is already at 2.5% and energy prices have not fully passed through to consumer prices yet. If the Hormuz situation persists and oil stays above $100, headline CPI will push toward 4% by May. Cutting rates into that environment would be a serious policy mistake. But holding rates while the economy softens risks tipping a scare into a confirmed contraction.

There is one important difference from the 1970s: the US economy is less energy-intensive than it was 50 years ago. Energy as a share of GDP is roughly half what it was in 1973. That limits the damage from an oil shock, but it does not eliminate it. A sustained shock above $120 per barrel will reach every corner of the economy through transport costs, food prices, and manufacturing inputs.

The Bottom Line

Stagflation is not confirmed yet. What is confirmed is that the conditions for it are forming. The trigger is the same as 1973: a geopolitical closure of a critical oil chokepoint. The Fed’s response options are the same: limited. Investors who think the Fed will ride to the rescue with rate cuts if markets fall further are reading the wrong playbook. Watch the CPI print this week. A number above 3.5% means the stagflation trade is no longer a tail risk. It is the base case.