Market Shock Survival Guide: What History Says to Do Right Now

Oil went from $73 to $119 and back to $87 in less than four weeks. The S&P 500 has swung hundreds of points on a single Trump press conference. Bond yields are rising while stocks are falling. If your portfolio feels like it is being managed by a weather machine, you are not imagining it. Markets are in shock mode, and the instinct to do something, anything, is exactly what gets most investors hurt. Here is what history actually says to do.

Not All Market Shocks Are the Same

The most important thing to understand about geopolitical shocks is that they split into two categories, and the right response depends entirely on which one you are in.

The first is a headline shock: markets panic, uncertainty spikes, investors sell first and ask questions later. These are fast and ugly but short. Research covering post-World War II geopolitical events shows an average peak-to-trough drawdown in the mid single digits, a bottom reached in roughly three weeks, and a full recovery in about six weeks. The Cuban Missile Crisis dropped markets 6.7% and recovered in 17 days. The 9/11 attacks caused an 11.9% drawdown that reversed in 30 days.

The second is a macro shock: the conflict lasts long enough to drive a sustained oil spike, which feeds inflation, forces central banks to tighten, squeezes consumer spending and corporate margins, and raises recession odds. That is how headlines become economics. The Iraq invasion of Kuwait in 1990 caused a 17.5% drawdown that took 187 days to recover. The 1973 Arab oil embargo produced a -37% real return over 12 months because oil prices did not normalise, they reshaped the entire macro regime.

What History Actually Looks Like

| Event | Max Drawdown | Days to Recover |

|---|---|---|

| Cuban Missile Crisis (1962) | -6.7% | 17 |

| 9/11 Attacks (2001) | -11.9% | 30 |

| Iraq Invades Kuwait (1990) | -17.5% | 187 |

| Pearl Harbor (1941) | -20.3% | 304 |

| Arab Oil Embargo (1973) | -37% real | 360+ |

Where This Conflict Sits on That Spectrum

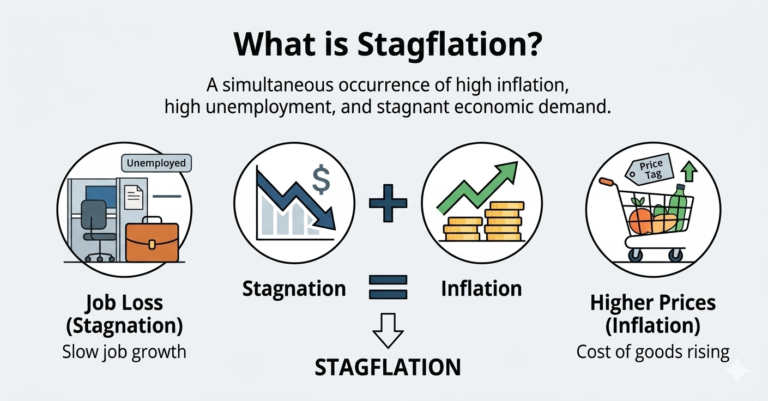

The Iran war has moved past the headline shock phase. The conflict has now entered its fourth week. The Strait of Hormuz, through which roughly 20% of global oil and LNG supply passes, remains effectively closed. Qatar has declared force majeure on LNG exports. Iraq has cut output by 70% at its three main oilfields. Oil spiked over 40% from pre-war levels. Eurozone PMI just hit a 10-month low on cost pressures. The ECB is now discussing rate hikes rather than cuts. These are the red flags that historically separate a recoverable shock from a macro event.

That does not mean 1973 is the template. Ceasefire talks are active. Trump has signalled the war is winding down. Oil has already given back a large portion of its gains. But Edmond de Rothschild Asset Management estimates that every $15 rise in oil adds 1 percentage point to inflation in developed economies while removing 0.3 to 0.4 percentage points from GDP growth. Oil is still $14 above its pre-war level. The macro damage is happening in real time.

“Materially reducing market exposure risks missing any sharp relief rally that could follow progress toward a settlement.”

John Wyn Evans, Head of Market Analysis, Rathbones

Five Moves That Hold Up in Both Scenarios

Whether this ends in six weeks or six months, the following positions make sense in either outcome.

-

1. Do not sell into the panicEvery major investment house says the same thing: reactive selling is the most reliable way to lock in a loss and miss the recovery. The relief rally when a ceasefire is announced will be sharp, fast, and it will not wait for you to re-enter.

-

2. Add inflation protectionTreasury Inflation-Protected Securities (TIPS) and inflation-linked bonds (linkers) hedge directly against the specific risk the Iran war creates. If central banks tolerate higher inflation to protect growth, linkers win. If they hike aggressively, short-duration bonds give you less exposure to rate risk than long bonds.

-

3. Energy equities are a direct hedgeOil companies profit when crude rises. If the Strait of Hormuz remains constrained, energy stocks continue to benefit. Shell and BP both held positive territory when the FTSE 100 fell 1.2% at the peak of the selloff. Energy equities do not solve the macro problem, but they offset some of the portfolio pain while it plays out.

-

4. Gold is doing what it is supposed toGold has low correlation to both equities and bonds during inflationary shocks. It does not pay a dividend and it is not a growth asset, but in an environment where the standard stock-bond portfolio is losing on both legs simultaneously, an uncorrelated asset earns its place.

-

5. Watch oil, not headlinesTrump’s statements move oil by 5% in a session. Iran’s denials move it back. The signal that actually matters is whether crude stays elevated for weeks, not whether Trump says the war is won on a Tuesday. If oil normalises toward $73 to $80, the macro shock is contained. If it holds above $90 for another month, revise your expectations.

The One Mistake That Keeps Repeating

In every major geopolitical shock, a significant number of retail investors sell near the bottom and buy back near the top of the recovery. The data is consistent across events. The reason is that the macro news gets worse before it gets better: PMI readings deteriorate, inflation data confirms the spike, central banks revise guidance. All of that happens while the market is already pricing in the resolution. By the time the news sounds good again, the recovery is largely over. The practical rule is simple: if you would not rebalance out of equities during a normal 5% correction, you should not rebalance during a geopolitical shock either. The shock is noisier, not fundamentally different.